Supply, Demand & Government Policies

This section examines how governments can implement policies to influence equilibrium price, equilibrium quantities, supply and demand in the market. These policies include adjustments to taxes, introduction of subsidies and the establishment of price controls. Throughout this chapter i will refer to feasible real life economic examples in order to demonstrate the impact of such policies on the economy.

Price Controls

One particular way in which the government can influence market equilibrium is through the setting of price controls. These price controls are government mandated minimum or maximum prices that can be charged for specified goods. Governments sometimes implement price controls when prices on essential items, such as food or oil, are rising rapidly [1]. Price controls can be implemented through either a PRICE CEILING or PRICE FLOOR.

PRICE CEILING

A price ceiling is a government fixed maximum price at which a particular good can be sold. For example gasoline / rent controls.

Example 1) Price Ceiling On Gasoline

Major increases in the price of gas since the turn of the century has left many people urging the government to establish a price ceiling on gas. However, the implications of such a policy in the United States when a maximum price was set for gasoline in 1973 and 1979 has meant today’s administrations have opted not to adopt a similar policy. When a price ceiling is set, a shortage occurs this is the primary reason a price ceiling on gas has been avoided in the 21st Century. A price ceiling must be placed below the natural market equilibrium to be effective. However, as a result of this move, there is a now a greater demand at this lower equilibrium price. Furthermore, the quantity supplied has fallen in response to the lower equilibrium price. Therefore setting a price ceiling on gas will cause quantity demanded to be greater than quantity supplied, thus creating a scarcity and encouraging black market gasoline activities, queues and commuting problems for consumers.

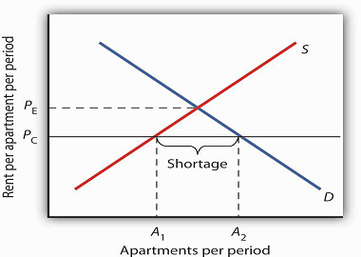

Example 2) Price Ceiling On Rent

There is two sides to the economic argument for and against implementing rent control. On one hand it is proposed a price ceiling on rents can create affordable housing. In contrast, many economists claim it is an inefficient way to try to raise the living standards of the poor in society.

SHORT RUN VS. LONG RUN

Short Run

Long Run

PRICE CEILING

A price ceiling is a government fixed maximum price at which a particular good can be sold. For example gasoline / rent controls.

Example 1) Price Ceiling On Gasoline

Major increases in the price of gas since the turn of the century has left many people urging the government to establish a price ceiling on gas. However, the implications of such a policy in the United States when a maximum price was set for gasoline in 1973 and 1979 has meant today’s administrations have opted not to adopt a similar policy. When a price ceiling is set, a shortage occurs this is the primary reason a price ceiling on gas has been avoided in the 21st Century. A price ceiling must be placed below the natural market equilibrium to be effective. However, as a result of this move, there is a now a greater demand at this lower equilibrium price. Furthermore, the quantity supplied has fallen in response to the lower equilibrium price. Therefore setting a price ceiling on gas will cause quantity demanded to be greater than quantity supplied, thus creating a scarcity and encouraging black market gasoline activities, queues and commuting problems for consumers.

Example 2) Price Ceiling On Rent

There is two sides to the economic argument for and against implementing rent control. On one hand it is proposed a price ceiling on rents can create affordable housing. In contrast, many economists claim it is an inefficient way to try to raise the living standards of the poor in society.

SHORT RUN VS. LONG RUN

Short Run

- Inelastic

- Consumers are unresponsive because they are not open to significant changes in living arrangements in the short term.

- Landlords have fixed units of housing and apartments and are therefore also unable to react in the short run to market changes.

Long Run

- Elastic

- As rents are now lower landlords are reluctant to build new housing units and struggling to keep up existing units.

- As rents are now lower the demand for housing rises particularly among first time buyers and also more housing is bought in city centre locations.

PRICE FLOOR

A price floor is a government fixed minimum price at which a particular good can be sold. For example a minimum wage.

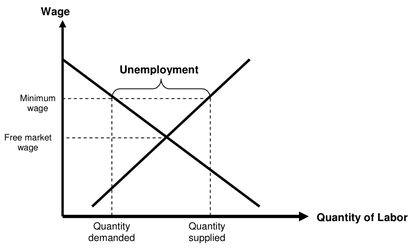

Example 1) A Minimum Wage

In a free labour market with no government intervention workers control the supply of labour and firms control the demand. The higher the wage rate, the greater the supply of labour. The higher the wage rate, the lower the demand for labour (all else being equal) [2].

A price floor is a government fixed minimum price at which a particular good can be sold. For example a minimum wage.

Example 1) A Minimum Wage

In a free labour market with no government intervention workers control the supply of labour and firms control the demand. The higher the wage rate, the greater the supply of labour. The higher the wage rate, the lower the demand for labour (all else being equal) [2].

However, if the government intervenes in the labour market by raising the minimum wage it will upset the balance between supply and demand in the market. When the minimum wage is raised above the equilibrium level the quantity of labour supplied is now greater than the quantity demanded. With a higher minimum wage the participation rate within the market will now rise. (The participation rate is the proportion of the population who are in the labour force). There is now a surplus supply of labour. Unemployment is the consequence, while the income of those workers in jobs will now rise. Those well-educated, highly skilled workers in the labour force will already be receiving a wage well in excess of the minimum wage so these workers will be unaffected by the change, it will be the lower skilled and teenage labour will experience these changes greatest. Finally, the effect of implementing a higher minimum wage also depends on the elasticity of the labour market. Where labour is relatively inelastic due to the high skill involved (eg.surgeon) unemployment and an income increase will be much less than where labour is elastic in a low skill industry (eg. Fast food restaurant cashier).

Taxes

Tax incidence is the manner in which the burden of a tax is shared among the participants in a market.

Tax Incidence On Consumer vs. Tax Incidence On Seller

|

Tax Incidence On Consumer

|

Tax Incidence On Seller

|

|

|

Subsidy

A subsidy is a payment to buyers and sellers to supplement income or lower costs and which thus encourages consumption or provides an advantage to the recipient. The primary intent of a government when levying a subsidy is to incentivise the consumption of a particular good or service, and these subsidies are generally given to sellers [3].

Example 1) Subsidy Levied on Dublin Bus

In order to encourage the use of public transport and reduce the amount of cars on our roads in an attempt to protect the environment through lower fuel consumption, it is perfectly feasible that the government may begin to introduce public transport subsidies in the coming years for companies such as the state owned Dublin Bus. . In contrast to a tax, subsidies reduce the cost of production and thus in turn cause the supply curve to the shift to the right. Such a subsidy would increase the supply and cause the supply curve of Dublin Bus to the right. Equilibrium Price would fall while equilibrium quantity of buses would rise as seen in the diagram below.

Example 1) Subsidy Levied on Dublin Bus

In order to encourage the use of public transport and reduce the amount of cars on our roads in an attempt to protect the environment through lower fuel consumption, it is perfectly feasible that the government may begin to introduce public transport subsidies in the coming years for companies such as the state owned Dublin Bus. . In contrast to a tax, subsidies reduce the cost of production and thus in turn cause the supply curve to the shift to the right. Such a subsidy would increase the supply and cause the supply curve of Dublin Bus to the right. Equilibrium Price would fall while equilibrium quantity of buses would rise as seen in the diagram below.

Bibliography

[1] http://www.investopedia.com/terms/p/price-controls.asp (Nov. 24 2013)

[2] O’Grady. (2002) Leaving Certificate Economics Revised & Updated, Ireland, Folens Publishers

[3] Mankiw, Taylor. (2011). Economics,Second Edition, United Kingdom, Cenagage Learning.

[Fig. 1] http://awesomecons.blogspot.ie/2012/10/rent-control-fair-or-unfair.html

[Fig. 2] http://www.economics.utoronto.ca/jfloyd/modules/sadl.html

[Fig. 3] http://www.policynote.ca/the-problems-with-the-textbook-analysis-of-minimum-wages/

[Fig. 4] http://www.bized.co.uk/virtual/dc/farming/theory/th5.htm

[Fig. 5] http://www.bized.co.uk/reference/diagrams/Decrease-in-Supply

[Fig. 6] http://www.bized.co.uk/virtual/dc/farming/theory/th12.htm

[2] O’Grady. (2002) Leaving Certificate Economics Revised & Updated, Ireland, Folens Publishers

[3] Mankiw, Taylor. (2011). Economics,Second Edition, United Kingdom, Cenagage Learning.

[Fig. 1] http://awesomecons.blogspot.ie/2012/10/rent-control-fair-or-unfair.html

[Fig. 2] http://www.economics.utoronto.ca/jfloyd/modules/sadl.html

[Fig. 3] http://www.policynote.ca/the-problems-with-the-textbook-analysis-of-minimum-wages/

[Fig. 4] http://www.bized.co.uk/virtual/dc/farming/theory/th5.htm

[Fig. 5] http://www.bized.co.uk/reference/diagrams/Decrease-in-Supply

[Fig. 6] http://www.bized.co.uk/virtual/dc/farming/theory/th12.htm

References

http:// www.economics.fundamentalfinance.com/price-ceiling.php (Nov. 24 2013)

Case, Fair, Oster. (2012). Principles Of Economics, Tenth Edition, United Kingdom, Pearson Education Ltd.

Parkin, Powell, Matthews. (2008). Economics, Seventh Edition, United Kingdom, Pearson Education Ltd.

Parkin. (2010). Economics, Ninth Edition, United Kingdom, Pearson Education Ltd.

Sloman, Wride, Garratt. (2012). Economics, Eigth Edition, United Kingdom, Pearson Education Ltd.

Basu. (2003). Readings in Political Economy, Oxford, Blackwell Publishing.

Case, Fair, Oster. (2012). Principles Of Economics, Tenth Edition, United Kingdom, Pearson Education Ltd.

Parkin, Powell, Matthews. (2008). Economics, Seventh Edition, United Kingdom, Pearson Education Ltd.

Parkin. (2010). Economics, Ninth Edition, United Kingdom, Pearson Education Ltd.

Sloman, Wride, Garratt. (2012). Economics, Eigth Edition, United Kingdom, Pearson Education Ltd.

Basu. (2003). Readings in Political Economy, Oxford, Blackwell Publishing.