Elasticity & Its Applications

By definition, elasticity is ‘a measure of the responsiveness of quantity demanded or quantity supplied to one of its determinants’ ;(Mankiw & Taylor, (2011:94)

The Elasticity of Demand:

- Elasticity allows economists to analyse supply and demand with greater precision.

- Elasticity measures how changes in market conditions can lead to a response in buyers and sellers, i.e. how much trade is affected by changes in market conditions.

- Price elasticity of demand : ‘a measure of how much the quantity demanded of a good responds to a change in the price of that good, computed as the percentage change in quantity demanded divided by the percentage change in price’ ;(Mankiw & Taylor,(2011:94).

The Elasticity of Demand:

- This is how demand responds to changes in determinants.

- We are all familiar with the term ‘I’ll wait to buy it until it goes on sale’ ~ The law of demand illustrates the concept that a fall in the price of a good increases the quantity that is demanded, and as the definition states, the price elasticity of demand measures how much a change in the price of a good affects the quantity that is demanded.

- Goods can be placed in two categories; they are either ‘elastic’ or ‘inelastic’.

- Elastic goods are goods in which demand will vary significantly if the price changes - for example if the price goes down then the demand will go up. The level of income of a person, the price of the good in relation to the market price of other similar products and the availability of perfect or close substitutes are a few things that greatly influence goods which are elastic.

- Inelastic goods are goods that do not have a perfect (if any) substitute. Therefore if there is a vary in the price of the good (either up – due to an increase in tax per say or down) there will be no real vary in the demand for the product. Inelastic goods are goods such as lifesaving medicines, tobacco and petrol – there are no real substitutes for these goods and they are needed, so the demand for these goods will not change despite an increase or decrease in the price. For this reason, these goods are often taxed very heavily by the government.

http://flagpedia.net/currency/euro

‘Necessities’ versus ‘Luxuries’ :

The Effects of Time on the Elasticity of a Good:

The Importance of Elasticity to Firms and Governments:

Government Intervention in the Market:

Calculating the Price Elasticity of Demand:

The Percentage Change in Price (P)

- A factor which greatly affects the elasticity of a good is income levels, and therefore the concept of ‘necessities’ versus ‘luxuries’. People need ‘necessities’ to live – such as food but can choose not to buy, and do without ‘luxuries’.

- John Stuart Mill essentially described the demand for necessities like bread as inelastic: "There are many articles for which it requires a very considerable rise of price materially to reduce the demand; in particular, articles of necessity, such as the habitual food of the people in England, wheaten bread: of which there is probably almost as much consumed, at the present cost price, as there would be with the present population at a price considerably lower." ;(Mill,1909, first pub.1848).

- Generally speaking, specific markets tend to be more elastic then broad markets. For an example; take shoes. There is no substitute for shoes in general; they are needed to protect our feet. In this sense, they are an inelastic good. However from the ‘specific market’ perspective, they are a more elastic demand because there are so many different types of shoes, and therefore there are many substitutes – the only real difference is the price.

The Effects of Time on the Elasticity of a Good:

- When viewing the supply and demand if goods in terms of elasticity, it is important to keep in mind the concept of time. Goods which may be seen as inelastic may transition to being elastic over a period of time if the price of the good rises substantially.

- For example, if there is a rise in the price of tobacco, there will be no change initially in the demand of tobacco as it is an inelastic good, and there are no perfect substitutes for smokers. Nonetheless, over a few years, some people may not be able to afford the high prices and decide to cut back and smoke less frequently or quit altogether, or encourage some to not take up smoking at all, and the demand for tobacco may gradually decrease. Thus making tobacco an elastic demand.

The Importance of Elasticity to Firms and Governments:

- The concept of elasticity is important to firms and governments because it allows them to calculate how much an increase or decrease in the price of a good will affect the total revenue of the company – i.e. how much they will profit.

- For example, an increase in the price of an elastic good due to an increase in the tax, will affect the quantity of the good which will be demanded by consumers. In this case it is up to them to decide whether they can justify an increase in the tax and risk the decrease in demand for the good.

- An increase in the tax of an inelastic good would increase the total revenue because there would be no real change in the demand for the good despite the tax increase.

- As David Ricardo, a British economist in the 19th century said, ‘Taxes on luxuries have some advantage over taxes on necessaries. They are generally paid from income, and therefore do not diminish the productive capital of the country. If wine were much raised in price in consequence of taxation, it is probable that a man would rather forego the enjoyments of wine, than make any important encroachments on his capital, to be enabled to purchase it. They are so identified with price, that the contributor is hardly aware that he is paying a tax. But they have also their disadvantages. First, they never reach capital, and on some extraordinary occasions it may be expedient that even capital should contribute towards the public exigencies; and secondly, there is no certainty as to the amount of the tax, for it may not reach even income. A man intent on saving, will exempt himself from a tax on wine, by giving up the use of it. The income of the country may be undiminished, and yet the State may be unable to raise a shilling by the tax.’ ;( Ricardo,1817)

Government Intervention in the Market:

- Some governments believe that some things (basic necessities such as petrol) should be affordable to all, as income is unevenly distributed, so people should be able to afford these basic goods at a reasonable price.

- As such, they may intervene in the free market and set a maximum price that a good could be valued at ( this is known as a price ceiling ) and a minimum price that a good could be valued at (this is known as a price floor).

Calculating the Price Elasticity of Demand:

- Economists calculate the price elasticity of demand by dividing the percentage change in the quantity demanded by the percentage change in the price.

The Percentage Change in Price (P)

- It is important to remember that there is a negative relationship between the quantity demanded and the change in price, therefore they will always have opposite signs.

- Price elasticity’s of are often times recorded as negative numbers, it is a common practice to remove the negative sign in the answer and take the absolute value of the number.

- Greater price elasticity implies a greater response of quantity demand to price.

- When calculating the price elasticity of demand between two points on a demand curve, you may realise that the slope of the line is not a useful measure of the responsiveness of the good to increases or decreases in its price.

- For example you could come across two demand curves with very different numerical values for their slopes but they represent the same behavior.

- To solve this problem, some use the ‘midpoint formula’ which is calculating a percentage change and dividing it by the initial and final values.

- In other words, calculate the price elasticity of demand by converting the changes in price and demand to percentages. This gives us a common unit of comparison that is not affected by the unit of measurement which is being used.

- Price elasticity of demand is described as being the ‘The ratio of the percentage of change in quantity demanded to the percentage of change in price; measures the responsiveness of quantity demanded to changes in price’ ;(Case, Fair & Oster, 2009:123)

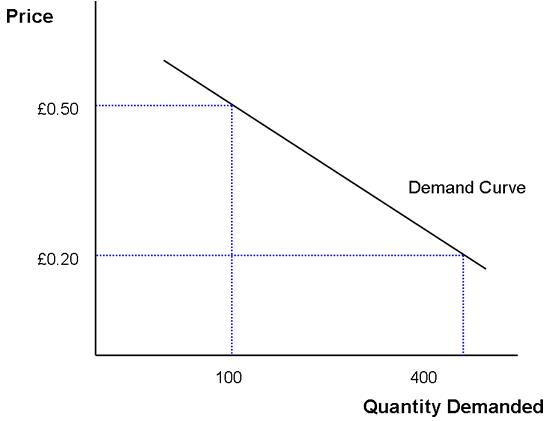

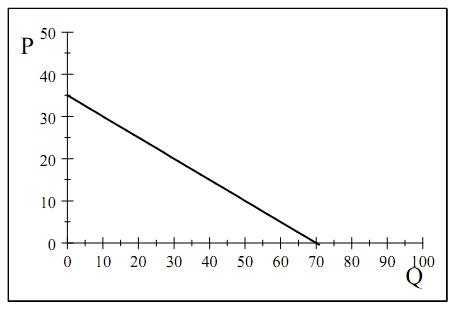

- Below is an example of a normal, straight line demand curve.

http://www.tutor2u.net/economics/gcse/revision_notes/demand_supply_demand_intro.htm

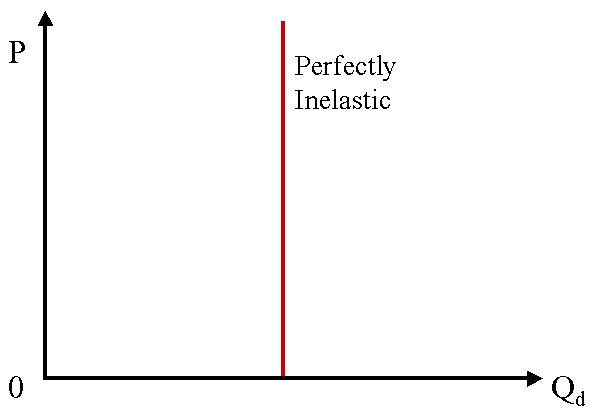

A ‘Perfectly Inelastic’ Good:

- If from your calculations, you find that there is a price elasticity of demand of zero, this means that the good is inelastic, i.e. that the quantity demanded is not affected by a change in the price of the good. If the elasticity is zero then the good is known as ‘perfectly inelastic’ and it can be concluded that the quantity demanded is fixed.

- Below is an example of a demand curve representing a ‘perfectly inelastic’ good.

http://wps.pearsoncustom.com/pcp_90734_uop_casefair/109/27997/7167315.cw/index.html

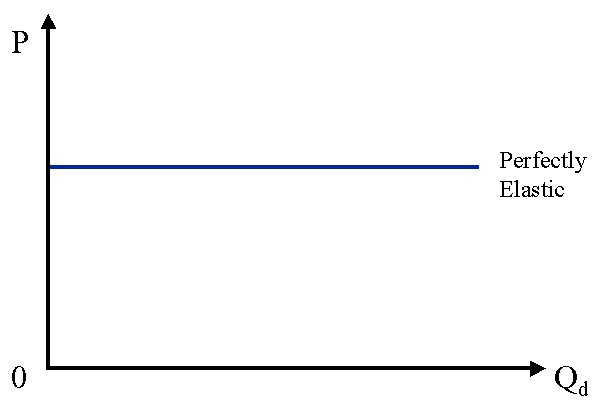

A ‘Perfectly Elastic’ Good:

- If there is a demand curve in which even the smallest increase in the price of a good reduces the quantity demanded to zero, then this good can be classified as being a ‘perfectly elastic’ good.

- For this type of good, firms can sell as much of the good that they want to for the market value, but even the smallest increase in its price will reduce the quantity demanded to zero. This is due to competition and the presence of perfect substitutes.

http://wps.pearsoncustom.com/pcp_90734_uop_casefair/109/27997/7167315.cw/index.html

Case Study of a ‘Perfectly Elastic’ Good:

- Two vendors – vendor A and vendor B are selling water and are set up at the finish line of a marathon. Say that both vendors are selling the exact same water for the same price – so they are receiving equal amounts of customers. If vendor A decides to raise the price of his water, his demand will instantly decrease to zero because everyone will start to buy from vendor B – who sells the water at market value. Therefore for the vendors, the smallest increase above market value will decrease the quantity demanded to zero, making this good a ‘perfectly elastic’ good.

- As we can see from the graphs, when the elasticity value is less than one, the demand can be described as being inelastic and the quantity changes more than the price.

- On the other hand, when the elasticity value is greater than one, the demand can be described as being elastic, and quantity therefore changes less than the price.

- When viewing demand curves therefore it can be concluded that; because the price elasticity of demand measures how much a change in the price of a good affects the quantity demanded, the flatter the demand curve, the greater the elasticity of the good represented on the curve (just as on the graph above we can see that the horizontal straight line through a given point represents perfect elasticity

- Furthermore, the steeper the demand curve, through a given point on the graph, the smaller the price elasticity of the good ( just as we can see from the examples above, the vertical line represents perfect in-elasticity)

http://vector-magz.com/search/free-vector-clipart-water-bottle/

Total Revenue of Price Elasticity of Demand:

- One of the most important factors that governments and firms examine with regard to price elasticity of demand is the total revenue. This is the amount which is paid by buyers and received by sellers for the good.

- This can be calculated by multiplying P x Q – the price of the good multiplied by the quantity of the good (which is sold for that price).

- Graphically, the total revenue can be calculated by multiplying the height of the box along the demand curve (P), by the width of the box under the demand curve (Q).

http://ingrimayne.com/econ/elasticity/RevEtDemand.html

- There are three general rules to remember when dealing with the total revenue of the price elasticity of demand.

1. If you have a price elasticity which is less than one, the demand curve is inelastic, an increase in the price will raise the total revenue and a decrease will reduce the total revenue because the demand never changes, but the price goes down so the seller is losing money.

2. If you have a price elasticity which is greater than one, the demand curve is elastic. An increase in the price will reduce the total revenue and a decrease in price will increase total revenue e.g. in a sale. The demand is easily changeable due to the availability of substitutes.

3. In a unique case of unitary elasticity, a percentage change in the price will cause an equal percentage change in the quantity demanded. In this case the price elasticity is equal to one, and a change in the price will not affect the total revenue.

Elasticity and Total Revenue Along a Linear Demand Curve:

% change in P

- When dealing with demand curves you may find that some will have an elasticity that is constant along the entire curve, for a linear demand curve, the elasticity will change along the line.

- It is important to remember that even is the slope of a linear demand curve is constant, the elasticity is not.

- This can be explained by the fact that the slope is the ratio of the changes between the variables of price and quantity. Elasticity is the ratio of the percentage changes in the variables of price and quantity.

% change in P

- This is a Linear Demand Curve:

http://www.tutorsglobe.com/homework-help/microeconomics/example-for-demand-function-73653.aspx

Case Study:

Say that for instance,you are the owner of a small cinema and you are running short of funds, the logical action to take would be to change the price of the admissions. The question is: do you raise or lower the prices?

If you lower the prices of admissions, you might have higher attendances, but for less money, whereas if you higher the prices, you may have lower attendances but for a higher price per ticket. The key thing to examine would be whether the demand for cinema tickets is elastic or inelastic.

If it was inelastic, you would raise your revenue because you would have a constant, fixed number of people paying for the tickets at a higher price.

If the demand was elastic, your number of admissions would fall if you raised the prices due to the competition of other cinemas that might charge less or offer a better deal.

In this case the clear solution would be to lower the prices for admissions, because your demand for tickets would increase and subsequently the increase in demand would override the loss in money for the cut in the price for the tickets.

It is also important in these circumstances to consider statistics – prices vs. admissions in other cinemas and prices vs. admissions in your cinema for previous years.

- The concept of price elasticity of demand is often used by companies such as museums of cinemas - for example when they are pricing admissions.

Say that for instance,you are the owner of a small cinema and you are running short of funds, the logical action to take would be to change the price of the admissions. The question is: do you raise or lower the prices?

If you lower the prices of admissions, you might have higher attendances, but for less money, whereas if you higher the prices, you may have lower attendances but for a higher price per ticket. The key thing to examine would be whether the demand for cinema tickets is elastic or inelastic.

If it was inelastic, you would raise your revenue because you would have a constant, fixed number of people paying for the tickets at a higher price.

If the demand was elastic, your number of admissions would fall if you raised the prices due to the competition of other cinemas that might charge less or offer a better deal.

In this case the clear solution would be to lower the prices for admissions, because your demand for tickets would increase and subsequently the increase in demand would override the loss in money for the cut in the price for the tickets.

It is also important in these circumstances to consider statistics – prices vs. admissions in other cinemas and prices vs. admissions in your cinema for previous years.

http://www.riverbendfilmfest.org/?page_id=9

Income Elasticity of Demand:

Likewise, if a persons income decreases, then their demand for 'normal' goods might decrease and they may resort to buying the ' inferior' goods in order to save money.

Cross Price Elasticity of Supply:

Percentage in Quantity Demanded of Good 2

Price Elasticity of Supply:

· Supply of a good is elastic if changes in the price cause a response in the quantity supplied.

· Supply is inelastic if a change in price causes only a small change in the quantity supplied.

· The price elasticity of supply is affected by the ability of producers to vary the amount of the manufactured good which is being produced.

- Income elasticity of demand is when economists measure how the quantity demanded of a good changes if peoples incomes change.

- This can be defined as 'a measure of how much the quantity demanded of a good responds to a change in consumers’ income,computed as the percentage change in quantity demanded divided by the percentage change in income'; (Mankiw & Taylor, 2011:103).

- Again this is examining the concept of ‘luxury’ versus ‘necessity’

- It is usually luxuries that are cut if people have a decrease in their level of income and they are short of money i.e. for any necessities that may be elastic, they may find perfect substitutes for them for less money.

- The concept of 'Normal' versus 'Inferior' goods is also important when examining the effects that a persons income may have on their demand for certain products.

Likewise, if a persons income decreases, then their demand for 'normal' goods might decrease and they may resort to buying the ' inferior' goods in order to save money.

Cross Price Elasticity of Supply:

- The 'Cross Price Elasticity of Demand' is a measure of how much the change in the price of one good can affect the quantity that is demanded of another good.

- This is defined as 'a measure of how much the quantity demanded of one good responds to a change in the price of another good, computed as the percentage change in quantity demanded of the first good divided by the percentage change in the price of the second good' ;( Mankiw & Taylor, 2011:104).

- To calculate the cross price elasticity of demand:

Percentage in Quantity Demanded of Good 2

- Whether your answer will turn out to be positive or negative depends on whether the good is a substitute or a complement to another good.

- If the good is a substitute for another good, the cross price elasticity of demand will be positive because the goods will move in the same direction. For example, if the price of cinema tickets increases, people may decide to wait until it comes out on DVD to watch it instead. Therefore the demand for DVD players and DVD's will increase.

- On the other hand, if the goods are compliments to one another, then the cross price elasticity of demand will be negative, because a decrease in the demand for one will cause a decrease in the demand of the other. For example, the relationship between DVD's and DVD players - they are complements to one another.

Price Elasticity of Supply:

- There are many factors that can cause a company top increase the amount of the good that they supply: such as when the technology of the industry improves, when the price of the good rises, when the demand rises, or when their input prices of the goods that they need to produce the product fall.

- The definition of the price elasticity of supply states that: ‘price elasticity of supply is a measure of how much the quantity supplied of a good responds to a change in the price of that good, computed as the percentage change in quantity supplied divided by the percentage change in price.’ ;(Mankiw & Taylor, (2011:104)

· Supply of a good is elastic if changes in the price cause a response in the quantity supplied.

· Supply is inelastic if a change in price causes only a small change in the quantity supplied.

· The price elasticity of supply is affected by the ability of producers to vary the amount of the manufactured good which is being produced.

- Similar to price elasticity of demand, goods become more elastic over long periods of time e.g. it takes a few years for a company to downscale the quantity of its supply being produced.

To Calculate the Price Elasticity of Supply:

Price Elasticity of Supply = Percentage Change in Quantity Supplied (QS)

Percentage Change in the Price (P)

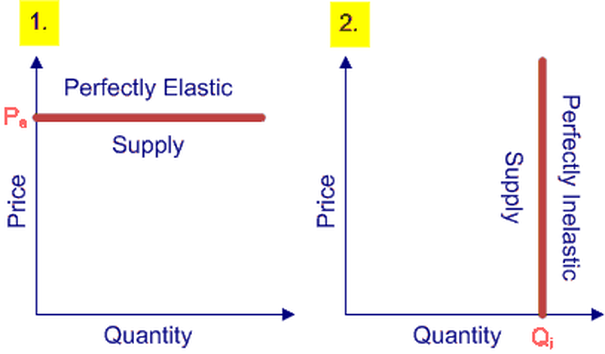

‘Perfectly Elastic’ and ‘Perfectly Inelastic’ Supply Curves:

- Formula Needed:

Price Elasticity of Supply = Percentage Change in Quantity Supplied (QS)

Percentage Change in the Price (P)

- Quantity responds to price in the supply curve.

- Similar to the demand curve, a vertical straight line represents a perfectly inelastic supply and a horizontal line represents a perfectly elastic supply.

‘Perfectly Elastic’ and ‘Perfectly Inelastic’ Supply Curves:

http://thismatter.com/economics/supply-elasticity.htm

- For ‘perfect in-elasticity’ supply, the elasticity = 0, and the quantity will be the same regardless of any changes in the price.

- For a ‘perfect elastic’ supply, elasticity = infinity, and very small changes in price lead to very large changes in the quantity supplied.

References

1. Case K.E, Fair R.C, & Oster S.M (9th edition) (2009) Principles of Economics, Pearson International Edition, Prentice Hall

2. Mankiw G.N & Taylor M ( 2nd edition) ( 2011) Economics, Cengage Learning

3. Marshall A (1920, first pub. 1890) Principles of Economics, Macmillan and Co. Ltd., London

4. Mill J.S (7th edition) (1909, first pub. 1848) Principles of Political Economy, Longmans, Green and Co., London

5. Ricardo D ( 3rd edition) (1817) On the Principles of Political Economy and Taxation, Murray J, London

2. Mankiw G.N & Taylor M ( 2nd edition) ( 2011) Economics, Cengage Learning

3. Marshall A (1920, first pub. 1890) Principles of Economics, Macmillan and Co. Ltd., London

4. Mill J.S (7th edition) (1909, first pub. 1848) Principles of Political Economy, Longmans, Green and Co., London

5. Ricardo D ( 3rd edition) (1817) On the Principles of Political Economy and Taxation, Murray J, London

Bibliography

1. Case K.E, Fair R.C, & Oster S.M (9th edition) (2009) Principles of Economics, Pearson International Edition, Prentice Hall

2. Importance of Elasticity, Wordpress, (Accessed on 1st November 2013)

Available from: http://economicsexposed.com/importance-of-elasticity/

3. Mankiw G.N & Taylor M ( 2nd edition) ( 2011) Economics, Cengage Learning

4. Marshall A (1920, first pub. 1890) Principles of Economics, Macmillan and Co. Ltd., London

5. Mill J.S (7th edition) (1909, first pub. 1848) Principles of Political Economy, Longmans, Green and Co., London

6. O’ Sullivan M.L (2013, last updated October 17th 2013) 40 Years After Embargo, OPEC is Over a Barrel, Available from:

http://www.bloomberg.com/news/2013-10-17/40-years-after-embargo-opec-is-over-a-barrel.html

(Accessed on 25th October 2013)

7. Ricardo D ( 3rd edition) (1817) On the Principles of Political Economy and Taxation, Murray J, London

8. Rose M (2003, last updated June 6th 2003) Elasticity and its Application, Library of Economics and Liberty, Available from: http://www.econlib.org/cgibin/printarticle2.pl?file=Columns/Teachers/elasticity.htm(Accessed on the 29th October 2013)

9. Stonebraker R.J ( last updated 17th May 2013) Elasticity of Supply and Demand, The Joy of Economics: Making Sense Out of Life, Winthrop University

Available from: http://faculty.winthrop.edu/stonebrakerr/book/elasticity.htm

(Accessed on 1st November 2013)

10. www.investopedia.com

2. Importance of Elasticity, Wordpress, (Accessed on 1st November 2013)

Available from: http://economicsexposed.com/importance-of-elasticity/

3. Mankiw G.N & Taylor M ( 2nd edition) ( 2011) Economics, Cengage Learning

4. Marshall A (1920, first pub. 1890) Principles of Economics, Macmillan and Co. Ltd., London

5. Mill J.S (7th edition) (1909, first pub. 1848) Principles of Political Economy, Longmans, Green and Co., London

6. O’ Sullivan M.L (2013, last updated October 17th 2013) 40 Years After Embargo, OPEC is Over a Barrel, Available from:

http://www.bloomberg.com/news/2013-10-17/40-years-after-embargo-opec-is-over-a-barrel.html

(Accessed on 25th October 2013)

7. Ricardo D ( 3rd edition) (1817) On the Principles of Political Economy and Taxation, Murray J, London

8. Rose M (2003, last updated June 6th 2003) Elasticity and its Application, Library of Economics and Liberty, Available from: http://www.econlib.org/cgibin/printarticle2.pl?file=Columns/Teachers/elasticity.htm(Accessed on the 29th October 2013)

9. Stonebraker R.J ( last updated 17th May 2013) Elasticity of Supply and Demand, The Joy of Economics: Making Sense Out of Life, Winthrop University

Available from: http://faculty.winthrop.edu/stonebrakerr/book/elasticity.htm

(Accessed on 1st November 2013)

10. www.investopedia.com